10年前的那次欧洲主权债务危机,曾让原本凝聚强劲的欧元区遭遇困境。然而本周,欧盟达成7500亿规模复苏基金协议,被法国总统马克龙称为“自欧元创建以来欧盟最重要的时刻”,欧元因此应声大涨。

在过去的12年中,欧元区一直背负着巨大的压力,而这一切都是从金融危机之后开始的。

金融危机过后,他们所面临的考验是寻找一种能够满足所有欧元区国家需求的解决方案。这并不是一件容易的事,因为各国都有自己的需求。有些国家急需更多的刺激措施,而有些国家则并不太需要,因此需求最少的国家并不想要自掏腰包,去资助那些“扶不起的阿斗”。

Over the last 12 years the Eurozone has come under enormous pressure. This kickstarted after the financial crisis whereby the collaborative group came under the unenvied test of finding one solution to meet the needs of all countries within the group. This is no easy task as countries naturally have their own needs to deal with. Some needed more stimulus, some less, those who needed the least didn’t want to put their hand in their pocket, funding those who they perceived to be less economically frugal.

于是,这必然会导致国家合作不畅的问题。曾几何时,人员自由流通、自由贸易和金融业的繁荣让各国凝聚在一起,然而当大家都面临困境时,内讧暗斗就悄悄开始了。正因如此,欧元区也更晚从金融危机中走出来。哪怕是在制造业和工业方面的超级大国德国,也是艰难克服这些压力。如此情形下,投资者纷纷将资金撤出欧洲,观望等待明显的上升趋势出现。

Therein lies the problem of a collaboration of nations, at times the freedom of movement, unified trade deals and financial power will work in favor, but when things turn tough the in fighting begins. Because of this, the Eurozone was slower to emerge from the crisis. Even the superpower of manufacturing and industry, Germany struggled to overcome these pressures. This scared investment out of the bloc as investors awaited a significant turn to the upside.

正是因为欧盟内部的压力、承诺和制约因素,英国全民公投做出了“脱欧”的决定,并将在2020年底前正式离开欧盟。这样的选择最终是对是错仍有待讨论,但自从新冠病毒的传播在英国造成冲击以来,人们越来越担心,英国是否有能力应对无协议脱欧的后果。

The internal pressures, commitment and constraints of the European Union is what brough the voters of the UK to vote to leave the EU, which remains on course to occur by the end of 2020. Whether that elects to be the right or wrong decision remained to be seen at the start of the year, but since the emergence of Covid-19 the strength of the UK to deal with no trade agreement and WTO terms is certainly a concern, should it transpire.

但对于欧元区来说,不同寻常的是,应对新冠疫情的成果让投资者们再一次相信了欧元区的实力。作为西方国家中最早受到病毒冲击的地区之一,欧洲中部各国迅速作出了反应,实行边境封锁,限制居民出行,并暂停公司营业。起初,这一较为激进的举措立刻让欧元和欧洲市场承受巨大压力。

But for the Eurozone, in the strangest of ways, the handling of the pandemic effects could prove to be the turning point in the investment communities believe in the collective bloc again. Being one of the first areas in the western world hit by the virus, Central Europe was quick to lock down its citizens, businesses, and borders. The immediate shockwaves of this drastic action bore pain on the Euro and European Markets.

在较长一段时间的封锁措施过后,事实证明,这样的措施比英国和美国采取的应对方法更加有效。尽管我们都清楚,面对新冠病毒,一切皆未可知,然而我们的确明显看到了欧洲的恢复。

Lockdown was maintained for a prolonged period, and so far, the results of this seem to have been successful in comparison to the US and UK. Whilst as we know with Covid-19 nothing can be a given, but the signs are certainly strong for a good recovery.

欧元区接下来又面临了另一个危机,那就是如何从财政援助和刺激手段的角度出发,共同寻求一个解决方案。在过去的一个月里,人们一直在猜测欧盟是否有能力达成协议。

From a financial aid and stimulus perspective, we were faced with another financial crisisesque scenario, whereby a collective solution was required for a situation that hit and effected more countries than others. Over the last month speculation had been gathering about the bloc’s ability to find agreement.

然而就在本周,欧盟决议通过将设立7500亿欧元的经济复苏基金,其中包括了3600亿欧元的低利率贷款发放以及3900亿欧元的救助金。这对于欧元区来说,意味着跨出了非常重要的一步。法国总统马克龙称,这是自欧元创建以来欧盟最重要的时刻。

However, earlier this week the EU agreed a 750 billion recovery plan via 360 billion of low interest rate loans and 390 billion of grants. This was a huge step forward and heralded as one of the most important steps since the inception of the Euro by French President Macron.

因此,本周的新闻头条都围绕在欧洲积极应对新冠以及欧盟达成救助计划协议的利好消息上,欧元因此强劲反弹。那么问题来了,欧元的大涨是否只是昙花一现?

So, whilst this weeks headlines focuses on Europe’s positive handling of the pandemic and ability to find mutual agreement in the rescue package, the Euro currency saw a relief rally. The question is will that just be a flash in the pan before a downward correction?

如前所述,欧元此前并不是货币持有者、投资者和基金的第一选择。那么,增加欧元配比的投资组合调整或许是能够解释欧元上涨的原因,并且这样的影响将在未来持续较长一段时间。

As stated, the Euro hasn’t been the holding of choice for reserve currency holders investors and funds, so perhaps we now have a reason for portfolio shifts which could raise the value, over not just a few days but a significant period.

在美国,特朗普希望弱化新冠所带来的影响,并拼命地鼓吹股票市场,从而成为他用于总统选举的“独特卖点”,这一切都引发了担忧。另一方面,人们同样担心一旦民主党候选人成功当选总统,那么将进入加税周期。英国则尚未完全解除封锁状态。英美两国不稳定的情形,或许会导致投资者兴趣的转移,甚至将投资带回新兴市场。

With the US and Trump looking to have underestimated the impacts of the virus and him being hellbent at inflating the equity market to create a USP for his ailing election campaign there are concerns in the US. There is also concerns over the tax implications should we see a Democrat President. The UK remains part cocooned and only just emerging from the homeward safety of lockdown. These factors could see a shift out of the US and UK and even bring investment back towards the Emerging Markets.

综合考虑上述各个因素,我们看到,投资者、企业和消费者信心指数均看好欧洲。德国达克斯指数就是最好的例子,在本周终于追回了新冠爆发以来的损失。

Considering the above factors, we are seeing investor, business and consumer confidence coming back towards Europe. A perfect example of this is the German stock market (DAX) which has this week finally recouped the losses brought by the pandemic.

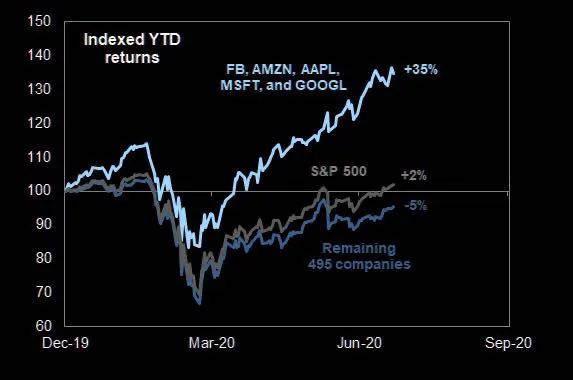

显然,美国的所有主要指数也已经达成了这一目标,但别忘了,美国市场是由少数公司所主导的,也是因它们出色的业绩而上涨;然而,德国的达克斯指数在板块和企业规模方面更加平衡,它所达到的“V型”反弹更令人钦佩,并能更好反映出整体经济形势。

Obviously in the US we have already seen all major indices already achieve this feat, BUT it must be considered that the US markets are enormously dominated by a handful of companies and the performance of the collective indices is dragged up by the few, whereas the German Dax has a greater balance of sectorial and equivalent business size contributors, making its “V shaped” recovery perhaps more admirable and reflective of the economy as a whole.

*美国市场的表现主要由少数的大公司所主导

综合考虑,在现在至美国大选结束前的时间段里,欧元可能将持续上涨,欧洲企业、商业及私人地产行业将蓬勃发展。

Considering the above there could well be a strong case for appreciation of the Euro and European Business, Commercial and Private Property Sectors as we come through the worst of the virus and past the US elections. The early indicators are perhaps already there to be seen.